This week’s financial news enters the first full week of June with jobs, inflation momentum, and earnings all jockeying for the driver’s seat.

Markets are weighing a firm PCE inflation read against a jobs-heavy calendar, plus policy headlines around Treasury issuance, budget talks, and oil. Geopolitical risks from the ongoing 2026 Iran conflict add another layer of uncertainty, with fragile ceasefire talks, intermittent Strait of Hormuz tensions, and potential oil supply disruptions continuing to influence energy markets. The mix can sway yields and sector leadership in a hurry. Below is a concise, web-friendly rundown of what matters now, what could move markets next, and how politics may shape the financial news narrative this week.

PCE, GDP, and Yields: Setting the Stage in Financial News

Disinflation has been uneven, with April PCE showing firmness (headline +3.8% YoY, core +3.3% YoY) while growth held steady in recent revisions. That combination keeps policy expectations in flux and tempers aggressive rate-cut hopes. The near-term test arrives through this week’s labor and activity data. Long yields tend to ease when wage pressure cools and services inflation drifts lower. That backdrop often helps housing, utilities, and select REITs.

Three portfolio takeaways after last week’s inflation and growth checkpoints:

- Lower long yields can broaden equity participation beyond a narrow leadership cohort.

- Intermediate duration regains hedging value if growth cools gradually.

- Quality still earns premium multiples—recurring revenue, margin discipline, and clean capital allocation matter most.

Energy remains the swing factor. OPEC+ signals, U.S. inventory trends, and developments in the Iran conflict (including Strait of Hormuz access) can nudge crude. Oil moves filter into headline inflation and, in turn, the rate path. That feedback loop changes sector tone quickly across refiners, airlines, transport, and consumer purchasing power. Politics adds another lever. Budget progress and Treasury issuance can shift the term premium. A smoother path typically calms long-end yields; a noisier one can keep them sticky a bit longer in the financial news cycle.

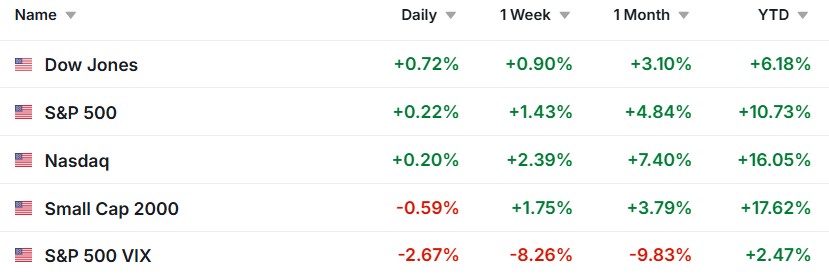

US Market Performance – Week Ending 5/29/26

Jobs Week, ISM, and Policy Currents in Financial News

Jobs week often sets the tone. Payrolls, unemployment, and wages will shape expectations for rate cuts and the direction of bond yields. A cooler but steady labor trend supports the soft-landing story. A hot wage surprise can complicate services inflation and keep higher-for-longer in play a bit longer.

What markets will watch most closely:

- Payrolls: Moderate job growth supports demand without reigniting inflation.

- Unemployment rate: Stability balances growth with disinflation progress.

- Average hourly earnings: Wages steer services inflation and the timing debate for cuts.

- Participation: Higher participation can relieve wage pressure at the margin.

Policy headlines still matter. Treasury auction sizes, the budget path, and tech oversight can move the term premium and valuation ranges. Trade and industrial policy can influence input costs and margins. The practical takeaway stays steady: pair selective growth with quality income, and keep some intermediate duration as a cushion against downside growth surprises. That balance helps when the financial news can change before lunch.

This Week: Key Economic Data

- Monday: ISM Manufacturing Index; S&P Global Manufacturing PMI (final); Construction Spending

- Tuesday: Job Openings and Labor Turnover Survey (JOLTS); Factory Orders; U.S. Treasury note auctions

- Wednesday: ADP National Employment Report; ISM Services Index; S&P Global Services PMI (final)

- Thursday: Weekly Jobless Claims; Productivity & Costs (revised); U.S. Trade Balance; Federal Reserve balance sheet

- Friday: Employment Situation Report (Nonfarm Payrolls, Unemployment Rate, Average Hourly Earnings); Consumer Credit

This Week: Companies Reporting Earnings

Retail, semiconductors, software, and specialty consumer names headline the early-June calendar.

- Broadcom (AVGO)

- Lululemon Athletica (LULU)

- Costco Wholesale (COST)

- MongoDB (MDB)

- DocuSign (DOCU)

- Chewy (CHWY)

- GameStop (GME)

- RH (RH)

- Dollar General (DG)

- Kroger (KR)

- Campbell Soup (CPB)

- AutoZone (AZO)

Q2 Estimated Taxes: June 15 Safe‑Harbor Check

The second quarterly estimated tax payment is due June 15 for many filers. To help avoid underpayment penalties, the IRS safe harbor generally requires paying at least 90% of this year’s total tax or 100% of last year’s tax (110% if prior-year AGI exceeded $150,000). Consider using the IRS Tax Withholding Estimator to tune paycheck withholding now and reduce the size of the June estimate. For fast, trackable payments, use IRS Direct Pay or EFTPS and save confirmations for your records.

This information is not a substitute for individualized tax advice. Please consult with a qualified tax professional to discuss your specific tax issues. Tip adapted from IRS.

Footnotes and Sources

- Bureau of Economic Analysis: Personal Consumption Expenditures (PCE) Price Index

- BEA: Economic release schedule (GDP; Personal Income & Outlays)

- Bureau of Labor Statistics: U.S. economic release calendar

- BLS: Employment Situation (payrolls, unemployment, wages)

- ISM: Manufacturing and Services Reports on Business

- U.S. Treasury: Daily yield curve and auction details

- U.S. EIA: Weekly Petroleum Status Report

- WSJ Markets: Earnings calendar

- CNBC Finance: Markets and financial news

- Bloomberg Markets: Global market data and analysis

- IRS: Estimated taxes and safe harbor rules

- IRS: Tax Withholding Estimator

Wesley Samson

Wesley@samsonfinancial.net

863-345-0538

Samson Financial, LLC.

https://www.samsonfinancial.net