Markets are watching the PCE inflation report, a fresh GDP estimate, and durable goods for clues on the path of rates. A packed earnings slate from software, chips, and hardware adds micro color to the macro picture. Budget headlines, Treasury supply, and oil prices remain the political and policy crosscurrents that can nudge yields and sector leadership. Here is a concise, web‑friendly guide to what matters now—and what could move markets next.

PCE And GDP Take Center Stage In Financial News

Two releases frame the week: the Personal Consumption Expenditures (PCE) Price Index and the second estimate of quarterly GDP. Together, they refresh the growth‑versus‑inflation debate and, by extension, rate expectations.

What matters most for markets right now:

- Core PCE trend. Cooling services inflation supports a steadier policy path and can ease long‑end yields.

- GDP composition. Consumer spending and business investment matter as much as the headline growth rate.

- Durable goods details. Transportation can swing the headline; core capital goods give a cleaner read on capex momentum.

- Housing sensitivity. Even modest rate relief can support builders and rate‑sensitive REITs, though affordability remains tight.

If disinflation continues without undercutting growth, the backdrop favors broader equity participation, steadier credit spreads, and some renewed hedging value from intermediate duration. If services inflation proves sticky, cash and short Treasuries keep their carry advantage a bit longer. Either way, quality—consistent free cash flow, margin discipline, and clean capital allocation—continues to earn premium treatment in this phase of the financial news cycle.

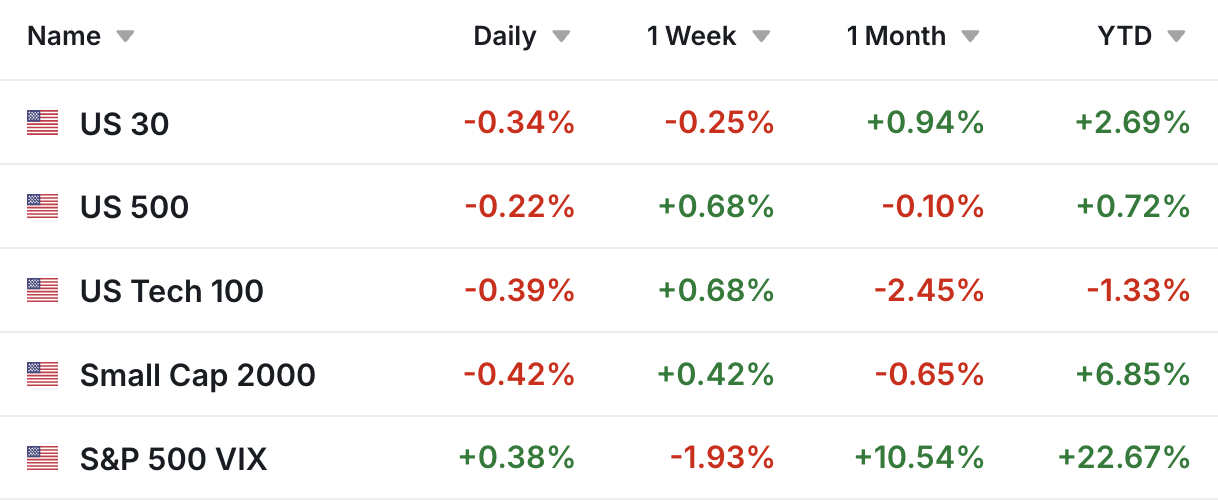

US Market Performance – Week Ending 2/20/2026

Policy, Oil, And Tech Oversight: Politics In Financial News

Politics is not the whole story. It still steers parts of it. The budget path and Treasury issuance can influence term premiums and rate volatility. A smoother funding backdrop tends to calm long yields. A choppier one can keep them sticky and multiples restrained.

Energy headlines remain a swing factor. OPEC+ communications and U.S. inventory trends can move crude. Oil swings filter into headline inflation and—by extension—rate expectations. That feedback loop touches refiners, airlines, transportation, and consumer purchasing power.

Regulatory scrutiny around large‑cap tech, data privacy, and AI governance can also nudge valuation ranges and capital return plans. The practical takeaway is steady: balance selective growth with quality income, keep some intermediate duration as a cushion against downside growth surprises, and diversify across size, style, and sector to reduce single‑policy risk. Markets may zig on Tuesday and zag on Thursday; a balanced plan travels better through the twists and turns of the financial news cycle.

This Week: Key Economic Data

Monday: New Home Sales (January); regional Fed manufacturing snapshots; Treasury bill auctions

Tuesday: S&P CoreLogic Case‑Shiller Home Price Index (latest monthly read); FHFA House Price Index; Conference Board Consumer Confidence (February)

Wednesday: Durable Goods Orders (January); EIA Weekly Petroleum Status Report; Pending Home Sales (January)

Thursday: Weekly Jobless Claims; Gross Domestic Product (Q4, second estimate); Chicago PMI (February)

Friday: Personal Income & Outlays (January) with PCE Price Index; University of Michigan Consumer Sentiment (final, February)

This Week / Next Week: Companies Reporting Earnings

Software, chips, and hardware headline the late‑February calendar. Here are the widely watched names due to report.

- Salesforce (CRM)

- Snowflake (SNOW)

- Workday (WDAY)

- HP Inc. (HPQ)

- Dell Technologies (DELL)

- Lowe’s (LOW)

- Target (TGT)

- Zoom Video (ZM)

- Autodesk (ADSK)

- Marvell Technology (MRVL)

- Best Buy (BBY)

- Monster Beverage (MNST)

Tax Tip: Clean Vehicle Credit At The Point Of Sale

Buying an eligible new clean vehicle? The federal Clean Vehicle Credit can be transferred to a registered dealer at the point of sale, effectively lowering the purchase price up front. Key rules apply: the buyer must meet income limits, the vehicle must meet eligibility and battery sourcing requirements, and the dealer must be enrolled with the IRS program. Keep the purchase documentation and the dealer’s credit transfer confirmation for records. When in doubt, verify eligibility using the IRS and Department of Energy resources before signing.

This information is not a substitute for individualized tax advice. Please consult with a qualified tax professional to discuss your specific tax issues.

Tip adapted from IRS.

Footnotes and Sources

- Bureau of Economic Analysis: Personal Consumption Expenditures (PCE) Price Index

- BEA: Economic release schedule (GDP, Personal Income & Outlays)

- U.S. Census Bureau: Manufacturers’ Shipments, Inventories, and Orders (Durable Goods)

- S&P CoreLogic Case‑Shiller Home Price Index

- FHFA: House Price Index

- The Conference Board: Consumer Confidence Index

- NAR: Pending Home Sales

- U.S. EIA: Weekly Petroleum Status Report

- WSJ Markets: Earnings calendar

- Bureau of Labor Statistics: U.S. data release calendar

- IRS: Clean Vehicle Credit and point‑of‑sale transfer

- DOE/IRS: Clean Vehicle Tax Credit resources (vehicle eligibility)

Wesley Samson

Wesley@samsonfinancial.net

863-345-0538

Samson Financial, LLC.

https://samsonfinancial.net