This Week’s Financial News: Post-Jobs Rate Expectations, FOMC Minutes, and Oil Headlines

Markets are digesting last week’s labor report, monitoring wage trends for signs of disinflation, and preparing for services data and the Fed’s March meeting minutes. Policy factors—including budget negotiations, Treasury supply, and energy policy—remain in the background and can affect the term premium and sector valuations. Below is a concise, web-friendly guide to what matters now, what to watch, and how these developments may impact portfolios.

Rates, Jobs, and the Fed: What’s Driving This Week’s Financial News

Rates continue to set the market tone. A cooler but steady labor market supports the soft-landing narrative and can push long-term yields lower. Hotter-than-expected wage growth, however, would complicate the services inflation picture and keep “higher-for-longer” expectations alive. The FOMC minutes from the March meeting will provide insight into how policymakers are weighing inflation progress against growth risks.

Practical read-throughs for positioning:

- Lower long-term yields tend to support housing, utilities, and select REITs.

- Persistent wage inflation would extend the carry advantage of cash and short-duration Treasuries.

- Intermediate-duration bonds can regain hedging value if growth cools gradually.

- Equity market breadth often improves when yields ease while earnings discipline remains strong.

Under the surface, stock selection remains critical. Markets continue to reward companies with recurring revenue, strong margin discipline, and consistent free cash flow. Firms with prudent capital allocation earn premium valuations, while those with unclear monetization paths often face rapid multiple compression. This selectivity defines the current phase of the market cycle.

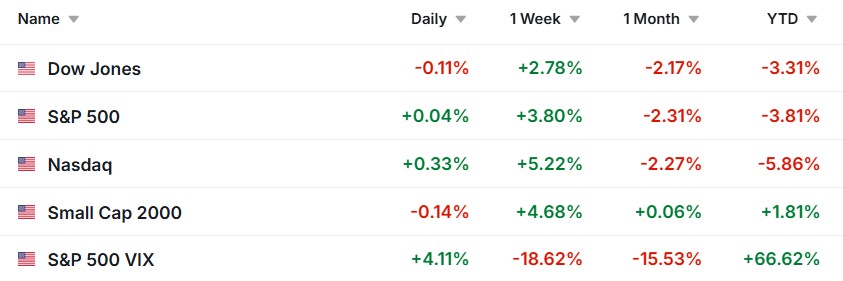

US Market Performance – Week Ending 4/3/2026

Policy Crosscurrents: Budget, Tariffs, and Oil in Financial News

Politics influences but does not dominate the story. Budget negotiations and Treasury issuance patterns shape the term premium and rate volatility. Smoother funding paths typically ease pressure on long-end yields and support risk appetite, while noisier developments can keep yields elevated and multiples in check.

Energy remains a key swing factor. OPEC+ signals and U.S. inventory data can move crude prices, which in turn feed into headline inflation and rate expectations. These swings affect airlines, refiners, transportation stocks, and broader consumer purchasing power. Trade policy, data privacy rules, and AI governance can also influence corporate cost structures and valuation ranges.

Practical takeaways:

- Balance selective growth exposure with quality income to mitigate single-headline risk.

- Maintain some intermediate-duration holdings as a buffer against further growth slowdowns.

- Diversify across company size, investment style, and sectors to navigate volatile news flow.

- Prioritize balance sheets with durable cash flows and disciplined capital returns.

This Week: Key Economic Data

- Monday, April 6: ISM Services Index (March); Treasury bill auctions

- Tuesday, April 7: Consumer Credit (G.19)

- Wednesday, April 8: FOMC Minutes (March 17-18 meeting); Wholesale Inventories; EIA Weekly Petroleum Status Report

- Thursday, April 9: Weekly Jobless Claims; Fed balance sheet

- Friday, April 10: University of Michigan Consumer Sentiment (preliminary April)

This Week: Companies Reporting Earnings

A relatively light week for major S&P 500 reports, but several notable companies are scheduled to release results. Key names include:

- Tuesday, April 7: Levi Strauss (LEVI) – after market close

- Wednesday, April 8: Delta Air Lines (DAL) – before market open; Constellation Brands (STZ) – after market close

- Thursday, April 9: WD-40 (WDFC) – after market close

Additional smaller or mid-cap reporters this week include Applied Digital (APLD), Aehr Test Systems (AEHR), BlackBerry (BB), Greenbrier (GBX), Neogen (NEOG), and others. Watch for commentary on consumer trends, fuel costs (especially for airlines), and forward guidance amid shifting rate expectations and oil price volatility.

File An Extension The Right Way Before Tax Day

Need more time to complete your return? File Form 4868 for an automatic six-month extension. Remember: an extension to file is not an extension to pay. To minimize or avoid penalties and interest, pay any expected tax balance when you file the extension—target at least 90% of the current year’s tax liability or use the safe harbor rule (generally 100% of last year’s tax, or 110% if your prior-year AGI exceeded $150,000).

Use IRS Direct Pay or EFTPS for fast, traceable electronic payments. If eligible, you can still make prior-year IRA or HSA contributions by the original federal filing deadline (April 15, 2026). Keep all electronic confirmations, and check your state’s extension rules, as they may differ.

This information is not a substitute for individualized tax advice. Please consult a qualified tax professional for your specific situation. Tip adapted from IRS.

Footnotes and Sources

-

- Federal Reserve: FOMC calendar, statements, and minutes

- ISM: Services Report on Business

- Bureau of Labor Statistics: U.S. data release calendar

- BLS: Job Openings and Labor Turnover Survey (JOLTS)

- Federal Reserve: Consumer Credit (G.19)

- University of Michigan: Surveys of Consumers

- U.S. Department of Labor: Unemployment Insurance Weekly Claims

- U.S. EIA: Weekly Petroleum Status Report

- U.S. Treasury: Daily yield curve rates and auction details

- IRS: About Form 4868 (Application for Automatic Extension of Time to File)

- IRS: Pay your taxes (Direct Pay, EFTPS, and other options)

- IRS: IRA contribution and deduction limits

- IRS Publication 969: HSAs and Other Tax-Favored Health Plans

Wesley Samson

Wesley@samsonfinancial.net

863-345-0538

Samson Financial, LLC.

https://www.samsonfinancial.net