Markets enter a pivotal stretch. Mega-cap results and energy majors report, the first read on Q1 GDP lands Thursday, and the Fed’s preferred inflation gauge (PCE) arrives Friday. Geopolitics and politics remain in the mix: dollar swap lines, Middle East risks, and a high-profile Fed chair nomination hearing all color the backdrop. The combination may tug yields, credit tone, and equity leadership—sometimes before lunch.

GDP, PCE, and Earnings: Growth vs. Inflation in Financial News

The late-April calendar places the growth–inflation balance back under the microscope. The advance read of Q1 GDP will show how consumer spending, inventories, and business investment stacked up. A day later, Personal Income & Outlays with the PCE Price Index will clarify whether disinflation is holding, particularly in services.

Three practical read‑throughs if disinflation continues while growth stays steady:

- Long yields can ease. That supports housing, utilities, and select REITs.

- Intermediate duration regains hedging value if growth cools gradually.

- Equity breadth can improve, especially if earnings guidance stays disciplined.

If services inflation proves sticky, higher‑for‑longer remains in the conversation. Cash and short Treasuries keep a carry edge. Under the surface, the market still rewards companies with recurring revenue, clean capital allocation, and consistent free cash flow. That selectivity has defined this phase of the financial news cycle.

Earnings will do heavy lifting for day‑to‑day moves. Tech and energy headline; payments, consumer bellwethers, and industrials round out the slate. Themes to watch:

- AI and cloud monetization: evidence over promises—backlog quality, renewal rates, and cash conversion matter.

- Margins and operating leverage: cost control and productivity drive valuation resilience.

- Capital returns: measured buybacks and sustainable dividends are favored over splashy headlines.

- Energy: refining margins, capex discipline, and outlooks tied to oil volatility will shape the sector’s tone.

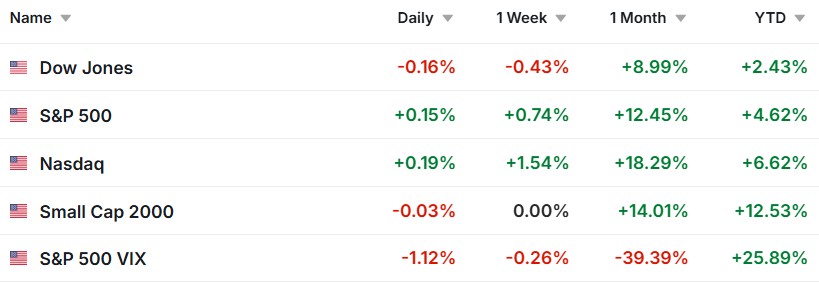

US Market Performance – Week Ending 4/24/2026

Policy, Oil, and the Dollar: Politics Reshapes Financial News

Policy is not the whole story, but it is steering key chapters. U.S. officials have defended dollar swap lines as the Iran conflict stresses global funding channels, a reminder that geopolitics can ripple through liquidity and currency markets. Oil remains the swing factor: OPEC+ signals and U.S. inventory trends can push crude, lift headline inflation, and nudge the term premium.

Another storyline: the Fed chair nomination. Betting markets now expect a Senate confirmation process to gather pace after separate legal clouds cleared, and hearing buzz has picked up. The path and tone of Fed leadership can influence forward guidance, rate vol, and term premiums—especially around the long end of the curve. The practical takeaway stays steady: balanced exposure across size, style, and sector helps cushion single‑headline risk in a fast‑moving financial news tape.

In short, this week’s financial news is a policy‑meets‑macro mash‑up. Growth and inflation prints set the baseline; earnings and oil decide the pace; politics can amplify the moves.

This Week: Key Economic Data

Monday: New Home Sales (Mar); Regional Fed manufacturing updates; Treasury bill auctions

Tuesday: S&P CoreLogic Case‑Shiller Home Price Index (Feb); FHFA House Price Index (Feb); Conference Board Consumer Confidence (Apr)

Wednesday: Durable Goods Orders (Mar); Pending Home Sales (Mar); EIA Weekly Petroleum Status Report

Thursday: Weekly Jobless Claims; Gross Domestic Product (Q1, advance); Chicago PMI (Apr)

Friday: Personal Income & Outlays (Mar) with PCE Price Index; Employment Cost Index (Q1); University of Michigan Consumer Sentiment (final, Apr)

This Week: Companies Reporting Earnings

The following widely watched companies are scheduled to report this week:

- Apple (AAPL)

- Amazon (AMZN)

- Exxon Mobil (XOM)

- Chevron (CVX)

- McDonald’s (MCD)

- Caterpillar (CAT)

- Starbucks (SBUX)

- Qualcomm (QCOM)

- Ford (F)

- General Motors (GM)

- UPS (UPS)

- Boeing (BA)

Q2 Estimated Taxes: Tune Up Before June 15

Quarterly taxpayers face a mid‑June deadline. To avoid underpayment penalties, the IRS safe harbor generally requires paying at least 90% of this year’s total tax or 100% of last year’s tax (110% if last year’s AGI exceeded $150,000). Consider using the IRS Tax Withholding Estimator to right‑size paycheck withholding now, reducing the need for larger estimates later. Electronic payments via IRS Direct Pay or EFTPS are fast and trackable—keep confirmations with your records.

This information is not a substitute for individualized tax advice. Please consult with a qualified tax professional to discuss your specific tax issues.

Tip adapted from IRS.

Footnotes and Sources

- CNBC Finance: Markets and financial news (swap lines, Iran backdrop, Fed chair hearing)

- Bloomberg Markets: Global data and analysis (rates, oil, sector moves)

- WSJ Markets: Earnings calendar

- BEA: Economic release schedule (GDP; Personal Income & Outlays/PCE)

- BEA: Personal Consumption Expenditures (PCE) Price Index

- Bureau of Labor Statistics: U.S. data release calendar (ECI)

- The Conference Board: Consumer Confidence Index

- S&P CoreLogic Case‑Shiller Home Price Index

- U.S. EIA: Weekly Petroleum Status Report

- U.S. Treasury: Daily yield curve rates and auction details

Wesley Samson

Wesley@samsonfinancial.net

863-345-0538

Samson Financial, LLC.

https://www.samsonfinancial.net